Image from pexels.com

Image from pexels.com

Related guides:

Key takeaways

- Understand the core concepts and terminology behind PCI DSS for Beginners: Get Compliant Without the Headaches.

- Learn practical steps to apply the guidance and stay audit-ready.

- See where SecureSlate can help centralize evidence, ownership, and ongoing compliance workflows.

If your business handles credit card transactions, you’re part of a system that millions rely on for secure financial interactions. Behind the scenes of every swipe, tap, and online checkout lies a framework called PCI DSS, short for Payment Card Industry Data Security Standard. It is like the blueprint for protecting sensitive cardholder data and avoiding the nightmare of data breaches and fines.

Established by major credit card brands like Visa, Mastercard, American Express, and Discover, PCI DSS sets the minimum requirements for data security. It’s not just for enterprise giants. Whether you’re a small online store or a global retail chain, compliance is non-negotiable if you deal with card payments.

Why Does PCI DSS Matter?

Because breaches cost more than money, they damage trust. In 2023 alone, the average cost of a data breach in the financial sector was $5.9 million , according to IBM. With phishing scams, ransomware, and insider threats on the rise, PCI DSS isn’t just a formality; it’s your shield.

What’s more, achieving compliance is often seen as a bureaucratic burden. But it doesn’t have to be. With the right knowledge and a clear plan, you can check every box, secure your customers’ data, and sleep better at night.

British Airways was fined £20 million in 2020 after a data breach exposed 400,000 customers’ payment details. While they were a big player, small businesses have also suffered devastating consequences. Hackers often target small merchants, assuming they lack strong security measures.

So, if you’re handling cardholder data in any form, you need to be PCI DSS compliant. And the sooner you start, the easier it is to scale securely.

Who Needs to Be PCI DSS Compliant?

A common misconception is that only large companies need to worry about PCI DSS compliance. In reality, any organization that stores, processes, or transmits cardholder data must comply, regardless of size or transaction volume.

Here’s who needs to comply:

- E-commerce websites accepting online credit card payments

- Retailers using POS (point-of-sale) systems

- Subscription-based services storing card details

- Hospitality providers with reservation systems

- Third-party payment processors

Even if you outsource payment processing to a gateway like Stripe or PayPal, you’re still responsible for how that data flows through your systems. PCI DSS mandates you to understand your scope and responsibilities, especially if you’re integrating with APIs or storing data, even temporarily.

The 12 Core Requirements of PCI DSS

At first glance, the PCI DSS framework might seem overwhelming. But once you break it down, the 12 core requirements become a practical guide to data protection.

Here’s a simplified view of the 12 requirements:

- Install and maintain a firewall : Acts as the first line of defense against unauthorized access.

- Do not use vendor-supplied defaults : Default settings are easy targets for attackers.

- Protect stored cardholder data : Use encryption, masking, and retention policies.

- Encrypt data in transmission : Especially over open or public networks.

- Use and regularly update antivirus software : Protect against malware and viruses.

- Develop and maintain secure systems : Patch vulnerabilities immediately.

- Restrict access based on need-to-know : Employees should access only what they need.

- Assign a unique ID to each user : Prevents shared credentials and enables tracking.

- Restrict physical access to data : Secure devices, servers, and documents.

- Track and monitor all access to network resources : Logging is crucial for audits.

- Regularly test security systems and processes : Includes vulnerability scans and pen tests.

- Maintain an information security policy : Set expectations, train employees, and review regularly.

Each of these requirements is designed to close a gap where attackers often sneak in. It’s not about adding friction, but it’s about fortifying your operations in a digital-first world.

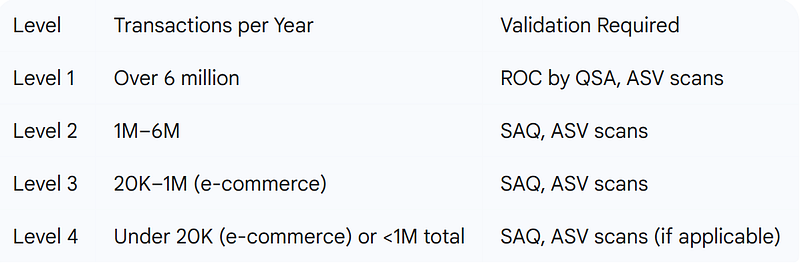

PCI DSS Compliance Levels and Validation

PCI DSS isn’t a one-size-fits-all standard. It recognizes that businesses differ in size and scope. That’s why there are four merchant levels , based on the volume of credit card transactions processed annually.

Overview:

- ROC (Report on Compliance) : A formal audit conducted by a QSA (Qualified Security Assessor).

- SAQ (Self-Assessment Questionnaire) : A series of yes/no questions that determine your level of compliance.

- ASV (Approved Scanning Vendor) Scans : Regular vulnerability scans to detect external threats.

Even if you’re a Level 4 merchant, taking the SAQ seriously is vital. Many small businesses mistakenly believe their size exempts them. But compliance isn’t optional, it’s contractual with credit card brands and acquiring banks.

Step-by-Step Guide to Becoming PCI DSS Compliant

This five-step roadmap will guide you to become PCI DSS compliant without stress:

1. Identify Your Scope

The first and perhaps most critical step is to accurately define the boundaries of your Cardholder Data Environment (CDE). The CDE includes any system, device, or process that stores, processes, or transmits cardholder data. Failing to identify all data touchpoints can lead to major compliance gaps.

Start by mapping out your entire data flow: how cardholder data enters your network (e.g., online payment gateways, POS systems), where it travels (servers, applications, APIs), and where it’s stored (databases, logs, backup systems). Include physical access points, remote systems, and third-party integrations.

The goal here is to narrow your PCI DSS scope as much as possible. By isolating and segmenting systems that handle payment data, you reduce the complexity of securing them, saving both time and cost.

2. Conduct a Gap Analysis

Once you understand your scope, it’s time to compare your current security posture against the 12 PCI DSS requirements. This step helps you discover where you’re already in good shape and where critical weaknesses exist.

For example:

- Do you have a firewall configured to industry standards?

- Are default system passwords still in place?

- Is sensitive cardholder data encrypted both at rest and in transit?

- Are all access logs being captured and reviewed?

- Are employees trained in handling payment data securely?

Use PCI DSS checklists, or better yet, a compliance management tool to help document this process. A gap analysis doesn’t just reveal technical deficiencies, it highlights operational vulnerabilities like outdated policies or insufficient employee training. The outcome of this step should be a detailed action plan prioritizing high-risk gaps for immediate remediation.

3. Remediate Security Gaps

Now that you know what’s broken, it’s time to fix it. Remediation is about aligning your systems, processes, and behaviors with PCI DSS controls. Depending on your gap analysis, you may need to:

- Install or update firewalls and intrusion detection systems

- Enable end-to-end encryption for data in transit

- Replace default credentials and restrict access using unique user IDs

- Deploy antivirus/malware protection and ensure it updates regularly

- Implement role-based access controls to enforce need-to-know policies

- Set up logging and monitoring across all in-scope systems

- Write and distribute a formal information security policy

One often overlooked area is employee training. Even the best tech stack fails if your team doesn’t know how to use it securely. Conduct phishing simulations, educate staff on secure password practices, and ensure everyone understands their role in protecting cardholder data.

How to Master ISO 27001 Gap Analysis: A Step-by-Step Starting Guide

Start ISO 27001 Now!

4. Complete the SAQ or Engage a QSA

This is the formal validation stage. Depending on your merchant level and environment type, you’ll either:

- Complete a Self-Assessment Questionnaire (SAQ) : This is a set of yes/no questions tailored to your specific business setup. There are multiple SAQ types (A, B, C, D, etc.), and choosing the right one is essential. For example, SAQ A is for businesses that outsource all card data functions, while SAQ D is for those that manage their own systems.

- Hire a Qualified Security Assessor (QSA) : If you’re a Level 1 merchant or handling large volumes of sensitive transactions, a QSA must perform an onsite assessment and create a Report on Compliance (ROC). A QSA brings expertise, validates your practices, and ensures your documentation and evidence are up to standard.

This step is where documentation becomes crucial. Save all your policies, logs, system configs, and training records, you’ll need them to prove compliance.

5. Submit Compliance Reports

After validation, it’s time to submit your compliance reports. Depending on your validation method, this could include:

- Your completed SAQ

- A Report on Compliance (ROC) from your QSA

- Attestation of Compliance (AOC)

- Results from ASV vulnerability scans

Submit these documents to your acquiring bank or card brand, typically on an annual basis. Keep in mind: even after submission, you must retain documentation for several years and remain prepared for potential audits or follow-up reviews.

Once submitted, don’t stop there. Use this milestone as the beginning of a culture of continuous compliance. Schedule regular reviews, adjust to new PCI DSS updates, and keep your security framework agile and responsive.

Tools and Technologies to Streamline PCI DSS

Tackling PCI DSS compliance manually can be a massive undertaking, especially for small and mid-sized businesses with limited IT staff. Fortunately, there are plenty of tools and technologies designed to streamline and automate much of the work involved.

Compliance Management Platforms

Solutions like SecureSlate, SecureTrust, Qualys, and Trustwave offer centralized platforms for managing every aspect of PCI DSS compliance. These tools often include:

- Automated SAQs tailored to your business type

- Real-time dashboards to track compliance gaps

- Remediation workflows and audit trails

Tokenization and Encryption Tools

Protecting cardholder data is at the heart of PCI DSS. Tools such as Thales CipherTrust , Protegrity , or VGS Vault provide tokenization and end-to-end encryption, reducing the risk of data theft while simultaneously shrinking your PCI compliance scope.

- Tokenization replaces cardholder data with random tokens, which are useless if stolen.

- Encryption ensures data remains unreadable during transmission or storage without the correct decryption key.

Vulnerability Scanning and Pen Testing Tools

Regularly testing your systems is required under PCI DSS. Solutions like Tenable , Nessus , and Rapid7 help identify weaknesses in your infrastructure. Working with an Approved Scanning Vendor (ASV) is a must for external vulnerability scans.

Logging and Monitoring Software

PCI DSS demands that all access to cardholder data and systems be logged and monitored. SIEM (Security Information and Event Management) tools like Splunk , LogRhythm , or IBM QRadar help centralize logs, detect anomalies, and alert on suspicious behavior.

These tools can reduce human error, improve documentation accuracy, and speed up audits. While they won’t guarantee compliance by themselves, they play a critical role in helping you build a secure and compliant environment.

Common Mistakes to Avoid During PCI DSS Compliance Process

PCI DSS compliance is full of moving parts, and many businesses fall into traps that delay certification, or worse, leave them vulnerable to breaches. Here are some of the most common missteps and how to avoid them:

Misunderstanding the Scope

Many businesses don’t correctly identify all systems that fall under PCI scope. If you’re transmitting cardholder data through a server, API, or third-party plugin, it’s in scope. Failing to map data flows accurately can expose hidden risks.

Assuming Outsourcing Equals Exemption

Using third-party processors like Stripe or Square doesn’t eliminate your responsibilities. You still must ensure they are compliant and understand how cardholder data interacts with your systems.

Ignoring Physical Security

Digital threats get all the attention, but PCI DSS also requires that physical access to cardholder data (servers, documents, devices) be controlled. Failing to secure access points, trash bins, and even printed receipts can lead to non-compliance.

One-and-Done Mentality

Compliance isn’t a one-time project. Some businesses treat PCI DSS like a checkbox exercise, only to discover gaps during an unexpected audit. Continuous compliance is the goal, through monitoring, policy reviews, and regular training.

Poor Documentation

Even if you’re technically compliant, poor or missing documentation can result in non-compliance during an audit. Keep clear, updated records of your policies, procedures, and security configurations.

Avoiding these mistakes helps not only with faster certification but also with building a truly secure and resilient operation.

The Cost of PCI DSS Non-Compliance

Ignoring PCI DSS compliance can lead to steep financial and reputational consequences. When cardholder data is compromised, you don’t just risk fines, but you risk your business’s future.

Financial Penalties

- Fines from credit card brands : Ranging from $5,000 to $100,000 per month depending on the severity and duration of non-compliance.

- Forensic investigation fees : Businesses are often responsible for paying for post-breach investigations.

- Chargebacks and card reissuance costs : You may also be liable for the cost of replacing compromised cards.

Operational and Legal Costs

- Civil lawsuits : If customer data is exposed, you could face class-action lawsuits.

- Increased transaction fees : Acquirers may raise your rates due to perceived risk.

Reputational Damage

According to a survey by Security.org, 31% of consumers said they would never do business again with a company that suffered a data breach. Trust takes years to build but seconds to destroy.

In 2013, Target suffered a breach that exposed 40 million credit and debit card records. It cost the company over $162 million , not including a massive dip in stock value and consumer trust. And Target was a major retailer with deep pockets. Imagine the impact on a small business.

Benefits of PCI DSS Compliance

It’s easy to view PCI DSS as just a set of rigid rules, but there are tangible business benefits to staying compliant, especially in today’s trust-driven marketplace.

Builds Customer Confidence

Displaying a PCI DSS compliance badge on your website or storefront tells customers their payment information is safe. This trust can increase conversion rates and reduce shopping cart abandonment.

Strengthens Cybersecurity Infrastructure

The requirements of PCI DSS firewalls, encryption, monitoring, etc., form a robust foundation for your overall security posture. They protect not just cardholder data, but also your company’s internal systems.

Competitive Advantage

In industries like e-commerce, SaaS, and fintech, being PCI compliant can be a competitive differentiator. Many enterprise clients won’t work with vendors who aren’t compliant.

Reduces Breach Costs

Studies show that compliant businesses suffer fewer and less costly breaches. A 2022 Ponemon Institute report found that organizations with mature compliance programs saved an average of $1.76 million per breach.

Simplifies Regulatory Overlap

Many PCI DSS controls overlap with regulations like GDPR, HIPAA, and CCPA. By complying with PCI, you’re also laying the groundwork for broader regulatory compliance.

How to Secure Data Privacy and Stop Breaches

Turn Your Privacy into a Powerful Brand Asset

PCI DSS Version Update

The PCI DSS framework is constantly evolving to stay ahead of cyber threats. In March 2022, PCI DSS version 4.0 was released, introducing several major changes:

What’s New in PCI DSS 4.0?

- Risk-based approach : Greater flexibility in how you meet requirements

- Enhanced authentication standards : Stronger focus on multi-factor authentication (MFA)

- More detailed logging and monitoring requirements

- Expanded encryption protocols and cloud security controls

Timeline for Adoption

- Until March 2025 : Businesses can still use PCI DSS 3.2.1

- After March 2025 : Full transition to PCI DSS 4.0 is required

Now is the time to review your current compliance program and begin aligning it with the new standards. Early adopters will be in a much stronger position to avoid disruptions and stay secure.

Conclusion

PCI DSS compliance doesn’t have to be intimidating. When broken down into practical steps and aligned with your business processes, it becomes a natural extension of your cybersecurity strategy.

By treating compliance as more than a regulatory burden, and instead embracing it as a business enabler, you protect your customers, build brand trust, and create operational resilience.

Start small, scope wisely, use the right tools, and don’t be afraid to call in the experts. Your reputation and your customers’ data deserve nothing less.

Ready to Streamline Compliance?

Building a secure foundation for your startup is crucial, but navigating the complexities of achieving compliance can be a hassle, especially for a small team.

SecureSlate offers a simpler solution:

- Affordable: Expensive compliance software shouldn’t be the barrier. Our affordable plans start at just $284/month.

- Focus on Your Business, Not Paperwork: Automate tedious tasks and free up your team to focus on innovation and growth.

- Gain Confidence and Credibility: Our platform guides you through the process, ensuring you meet all essential requirements, and giving you peace of mind.

Disclaimer (legal note)

SecureSlate is not a law firm, and this article does not constitute or contain legal advice or create an attorney-client relationship. When determining your obligations and compliance with respect to relevant laws and regulations, you should consult a licensed attorney.

Need compliance without the complexity?

SecureSlate automates ISO 27001, SOC 2, GDPR, HIPAA, and more. Built for growing teams. See it in action.

No credit card required

{kind=link}